When & How did Bitcoin come into existnce??

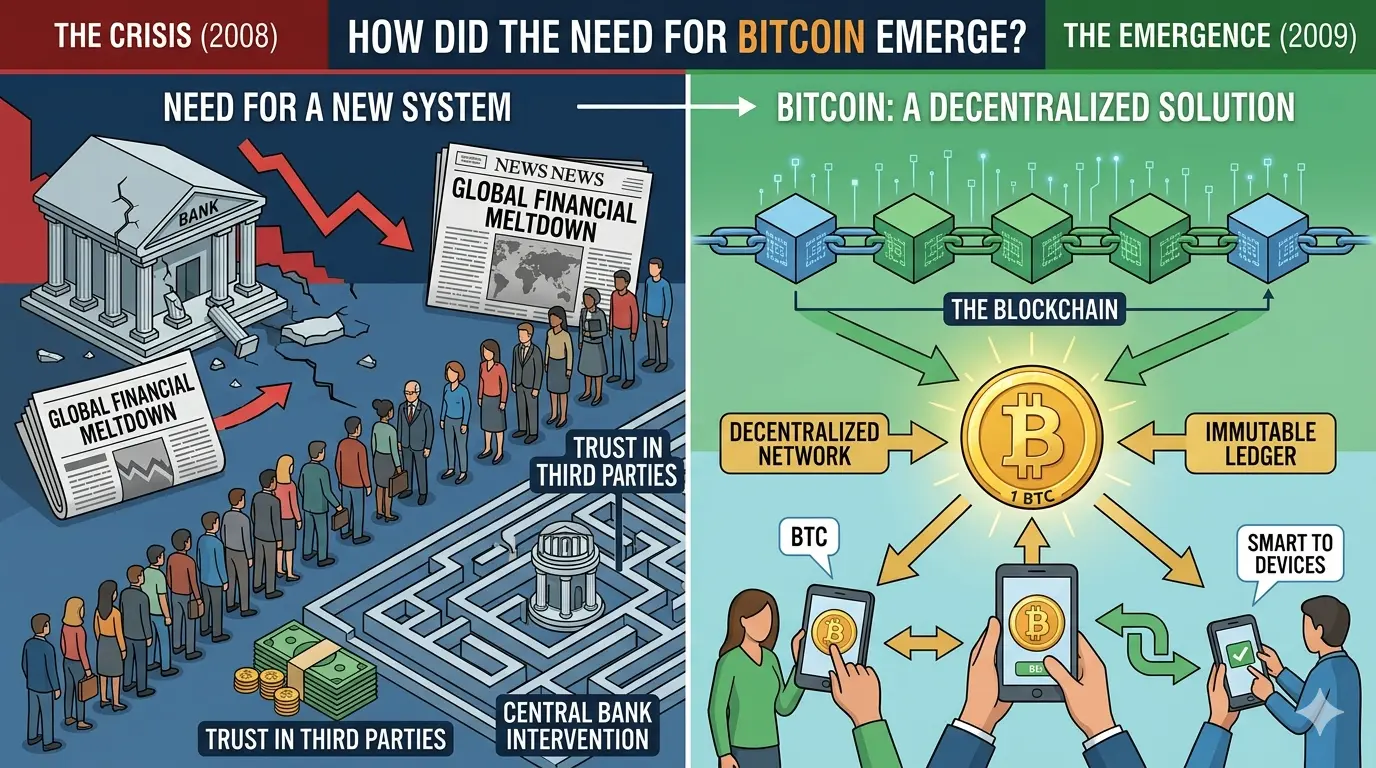

Bitcoin came into existence through the release of its whitepaper, Bitcoin: A Peer-to-Peer Electronic Cash System, by the pseudonymous Satoshi Nakamoto on October 31, 2008. It was published in response to the financial crisis, proposing a decentralized currency independent of central banks.

The network itself went live on January 3, 2009, when Nakamoto mined the genesis block (Block 0). Embedded in that block’s coinbase transaction was a permanent headline from The Times newspaper: “Chancellor on brink of second bailout for banks.” This timestamp served as both a proof of the launch date and a clear statement of intent—offering a trustless, peer-to-peer alternative to the traditional financial system.

For more details about about Genesis of Cryptocurrencies Click Here

Why do modern world need the Bitcoin?

The modern world needs Bitcoin primarily as a neutral, decentralized store of value and a trustless settlement network.

Unlike traditional systems, Bitcoin operates without central banks or governments. In an era of rampant inflation and monetary expansion, its fixed supply of 21 million coins offers a hedge against currency debasement—often called “digital gold.”

Beyond being an asset, it enables financial sovereignty. For individuals in countries with unstable currencies or restrictive capital controls, Bitcoin provides access to a global economy that cannot be seized or censored. It allows for permissionless transactions, meaning anyone with an internet connection can send value across borders without intermediaries, bank approvals, or lengthy delays.

Furthermore, Bitcoin’s proof-of-work mechanism provides unparalleled security and finality. As the world becomes increasingly digital, Bitcoin represents a foundational layer for property rights in the digital age—a neutral, verifiable, and immutable protocol that operates 24/7, independent of geopolitical instability or corporate insolvency risks inherent in traditional finance.

Possible negative outcomes of Bitcoin

Despite its benefits, Bitcoin carries significant negative outcomes.

Environmental impact is a primary concern. Its proof-of-work consensus requires immense energy consumption for mining, often relying on fossil fuels, raising serious sustainability issues.

Volatility and speculation make it unreliable as a stable currency. Wild price swings can lead to substantial financial losses for retail investors, while the market remains vulnerable to manipulation by large holders (“whales”).

Illicit use and security risks also persist. While not anonymous, Bitcoin has been used in ransomware attacks and darknet markets. Additionally, investors face permanent loss of funds due to lost private keys, exchange collapses (e.g., FTX), or sophisticated scams, with no centralized authority to offer recourse.

Finally, scalability and centralization pose challenges. The network processes far fewer transactions than traditional payment systems, and mining has become increasingly centralized among large industrial operations, contradicting its decentralized ideal.

Technology Behind the Bitcoin

Here is an explanation of the technology behind Bitcoin.

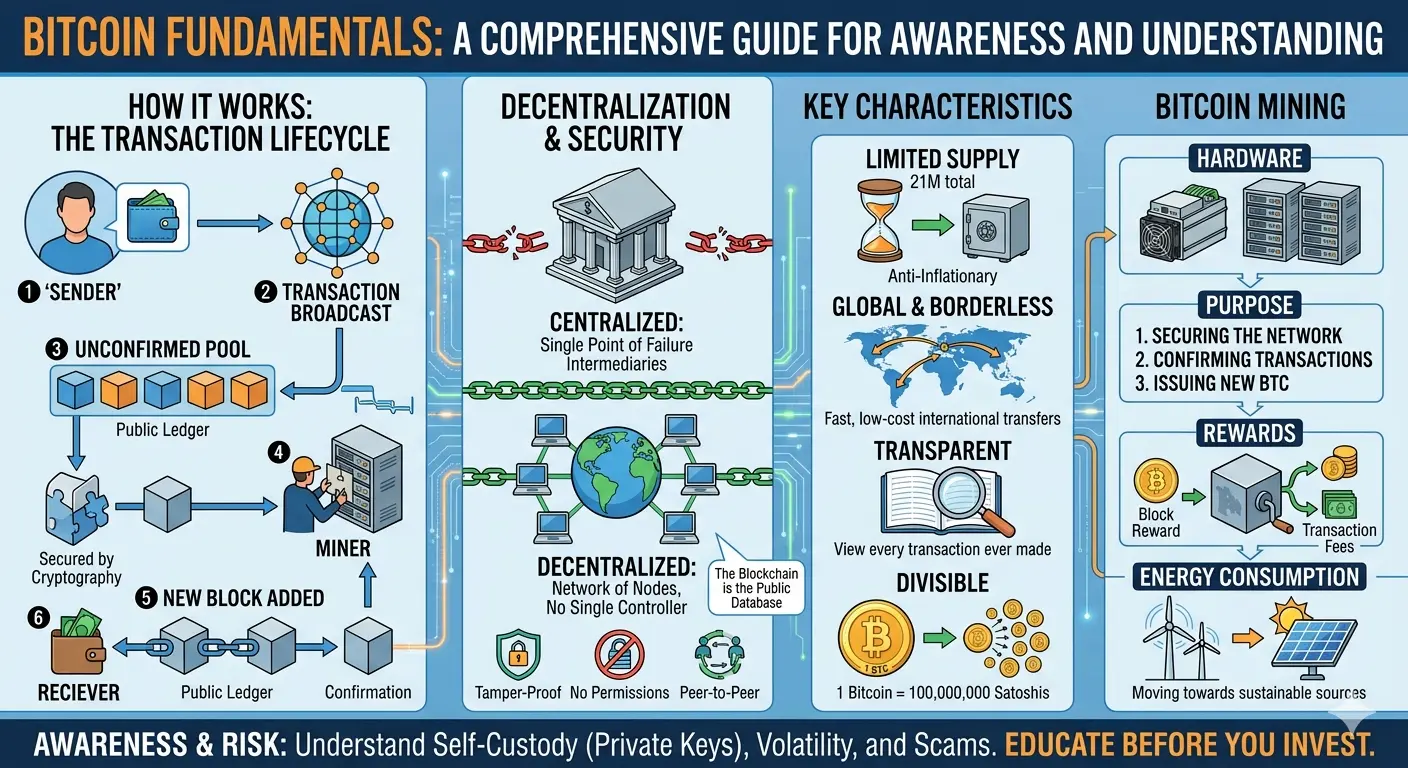

Bitcoin is often described as digital gold, but its true innovation lies not in the coin itself, but in the decentralized technological framework that supports it. At its heart, Bitcoin operates on a technology called the blockchain, a distributed public ledger that records every transaction ever made. Unlike a traditional bank ledger kept on a central server, Bitcoin’s ledger is replicated across tens of thousands of independent computers, or nodes, spread across the globe. This structure eliminates the need for a central authority, such as a bank or government, to verify and authorize transactions.

The Blockchain: An Immutable Chain of Blocks

The blockchain gets its name from its structure: it is a chain of data blocks, each linked to the previous one. A new block is created approximately every ten minutes and contains a list of recent, pending transactions. Each block also contains a unique cryptographic fingerprint called a hash, which is generated by running the block’s data through a mathematical function (SHA-256).

Crucially, each block’s hash is created using the hash of the previous block. This creates an unbreakable chain. If a malicious actor tries to alter a transaction in a block that was added three hours ago, that block’s hash would change instantly. Because the next block contains the original hash, the chain would break. To repair it, the attacker would have to re-mine that altered block and every single block that came after it—a feat requiring astronomical computational power. This property, called immutability, ensures that once a transaction is deeply buried under subsequent blocks, it is practically impossible to reverse.

Proof of Work: Reaching Agreement Without a Boss

The most revolutionary aspect of Bitcoin’s technology is how it achieves consensus among thousands of untrusted, anonymous nodes. How do all these computers agree on a single version of the truth? The answer is a mechanism called Proof of Work (PoW).

Specialized nodes known as miners compete to add the next block to the chain. To do so, they must solve a complex mathematical puzzle. The puzzle is a guessing game: miners take the pending block’s data, add a random number called a nonce, and run it through the SHA-256 hash function. The resulting hash must be below a certain target threshold (e.g., start with a specific number of zeros). Since there is no formula to predict the output, miners must trillions of guesses per second, burning significant electricity.

The first miner to find a valid nonce broadcasts their solution to the network. Other nodes can instantly verify the solution with a single hash calculation. If valid, the new block is appended to everyone’s copy of the blockchain, and the winning miner receives a reward (newly created bitcoins plus transaction fees). This process is called “mining” because it introduces new bitcoins into circulation, much like extracting gold from the earth.

Proof of Work serves two critical purposes. First, it makes attacking the network economically irrational. An attacker would need to control over 51% of the network’s total computing power to outpace honest miners—a prohibitively expensive endeavor. Second, it solves the “double-spend problem,” preventing someone from spending the same bitcoin twice, without requiring a central bank to validate the transaction.

Public-Key Cryptography and Ownership

While the blockchain tracks transactions, public-key cryptography determines who owns the bitcoins. Each user generates a private key (a secret, alphanumeric string) and a corresponding public key (derived from the private key). The public key is hashed to create an address, similar to an account number. The private key acts as a digital signature.

When you send bitcoin, your wallet software creates a transaction message and signs it with your private key. This cryptographic signature proves mathematical ownership of the funds without revealing the key itself. The network then verifies the signature using your public key. Anyone can see the transaction on the public ledger, but only the holder of the private key can authorize spending from that address.

The Longest Chain Rule

Finally, what happens if two miners solve a block simultaneously, creating two competing versions of the blockchain? The network resolves this via the longest chain rule. Nodes will accept the chain with the most cumulative Proof of Work (the greatest number of blocks mined). The shorter branch is orphaned and discarded. This elegant rule ensures that even with network delays and competing versions, the system inevitably converges on a single, agreed-upon history. This combination of cryptographic hashing, economic incentives, and distributed consensus enables thousands of untrusted computers to maintain a single, trustworthy, and global ledger without any central authority.

Mysterious Bitcoin Creator - Satoshi Nakamoto

The true identity of Satoshi Nakamoto—the anonymous creator of Bitcoin—remains one of the greatest unsolved mysteries in technology and finance. Between 2008 and 2010, Satoshi published the Bitcoin whitepaper, wrote the original software, and mined over one million bitcoins (worth tens of billions today), all while communicating only through encrypted channels and online forums.

What makes the mystery so profound is the deliberate vanishing. In late 2010, as Bitcoin began gaining serious attention, Satoshi handed the network alert key to developer Gavin Andresen, handed over control of the Bitcoin code repository to others, and then simply stopped posting. Emails to collaborators went silent. No explanation was ever given. Satoshi’s last known message in April 2011 stated simply, “I’ve moved on to other things.”

Numerous candidates have been proposed: Nick Szabo (creator of Bit Gold), Hal Finney (the first Bitcoin recipient), and even Dorian Nakamoto (a California engineer). Some have suggested groups, like the cypherpunk collective, or even government agencies. Each candidate presents compelling circumstantial evidence but lacks definitive proof, such as moving the original mined coins or possessing Satoshi’s known PGP keys. Notably, Satoshi’s fortune has never been touched—a fact that deepens the enigma.

The mystery endures because Satoshi designed Bitcoin to be trustless and decentralized. Ironically, the creator’s anonymity perfectly embodies that vision: Bitcoin does not need a leader, a face, or a god. Satoshi vanished to ensure the project could survive without them. Whether a single genius or a team, Satoshi Nakamoto is now both a person and a myth—a ghost whose legacy runs on 24/7, but whose identity may never be known.

Bitcoin - A Crime Coin - Myth vs Reality

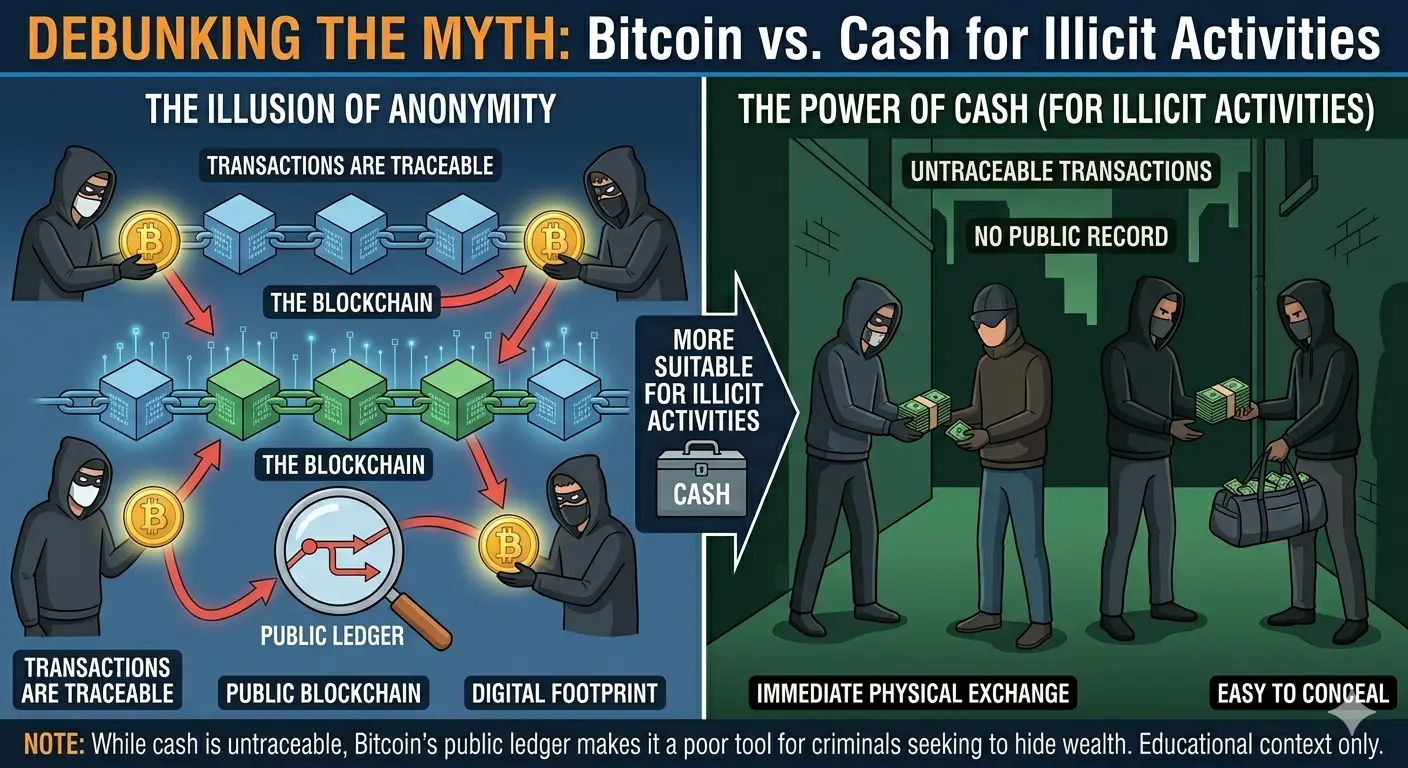

One of the most persistent yet misleading narratives about Bitcoin is that it serves as a haven for criminals. Early scandals like the Silk Road marketplace cemented this image of an anonymous, dark-web currency. However, this understanding is fundamentally backwards.

In reality, Bitcoin is the least suitable asset for illicit finance. Unlike physical cash or private bank ledgers, the Bitcoin blockchain is a permanent, public, and transparent record. Every transaction—from its origin to its current wallet—is traceable forever. Law enforcement agencies, including the FBI and IRS, have become highly sophisticated in blockchain forensics. They use commercial tools like Chainalysis to follow money trails, identify patterns, and unmask individuals through exchange records.

The irony is stark: physical cash remains entirely anonymous and untraceable, making it the true tool for illicit activity. Bitcoin’s pseudo-anonymity is a liability for criminals; a single mistake linking an address to an identity exposes their entire financial history. Consequently, the percentage of Bitcoin transactions linked to crime has fallen to under 0.5%—far lower than that of fiat currency. Rather than a criminal’s haven, Bitcoin has become an investigator’s ally, proving that public ledgers can be powerful tools for transparency and accountability.

The Energy Paradox : Wasteful or Grid Savior?

Bitcoin mining’s energy consumption—often compared to that of entire nations—is its most frequent criticism. The visceral image of server farms burning coal to solve meaningless puzzles suggests an environmental disaster. But this overlooks a revolutionary economic paradox: Bitcoin miners are the world’s ideal flexible energy buyer.

Unlike a factory or a data center, a Bitcoin miner can shut down instantly and restart just as fast, with zero product loss or safety risks. This unique property turns them into a “demand-response” resource. In places like Texas, miners buy excess wind and solar power when it’s abundant and cheap, and power down during peak grid stress, selling that reserved energy back to households. This stabilizes renewable grids and prevents curtailment (wasted green energy).

Even more striking is methane mitigation. Miners often set up mobile containers at oil fields, capturing natural gas that would otherwise be flared (burned wastefully) or vented (releasing methane, which is 80x more potent than CO2). They convert this stranded gas into electricity to mine Bitcoin, destroying methane in the process.

The paradox, therefore, is that Bitcoin’s seemingly wasteful energy appetite may actively subsidize renewable build-outs and lower global methane emissions—a twist that defies the simple “polluter” narrative.

Conclusion

Bitcoin emerged from the 2008 financial crisis as a radical answer to centralized failure—a peer-to-peer currency born from a whitepaper and an anonymous creator who then vanished. Today, its need in the modern world is clear: it offers censorship-resistant value transfer, financial inclusion for the unbanked, and a hedge against monetary inflation. Yet the path is not without perils. Its extreme volatility, regulatory uncertainty, and potential for user error remain genuine negative outcomes.

Beneath the surface, the technology—blockchain and proof-of-work—proves that trust can be coded, not commanded. And while early fears painted Bitcoin as a crime coin, the transparent ledger has flipped that narrative, making it a prosecutor’s tool rather than a criminal’s haven. Finally, the energy paradox refuses easy judgment: Bitcoin consumes power, but increasingly subsidizes renewables and mitigates methane waste. Love it or hate it, Bitcoin is no longer a question of “if.” It is a flawed, fascinating experiment whose final chapter is still being written.