The Pre-History & Philosophical Foundation (Pre -2008)

The Genesis : A Digital Cash Problem

Before Bitcoin’s invention in 2008, creating a purely digital currency faced a fundamental obstacle known as the double-spending problem. Unlike physical cash, digital files can be copied infinitely. This meant a malicious user could spend the same digital coin with multiple vendors before the system could detect the fraud.

Early innovators like David Chaum (DigiCash, 1989) solved this by creating centralized systems. A trusted bank or server acted as a central ledger, verifying transactions to prevent double-spending. While functional, this reintroduced traditional financial control—the very issue cryptography aimed to eliminate—as the central authority could freeze funds, reverse transactions, or be a single point of failure.

The Cypherpunk Movement : Privacy ,Encryption ,and Decentralization

The Cypherpunk Movement emerged in the late 1980s as a grassroots collective of cryptographers, activists, and technologists united by a radical belief: that strong cryptography and decentralized systems could protect individual liberty in the digital age. Spearheaded by figures like Eric Hughes, Timothy May, and Phil Zimmermann, they argued that as life moved online, privacy would disappear unless citizens actively built tools to defend it.

Their core philosophy rested on three pillars:

Privacy: Defined not as secrecy, but as the right to control one’s own data.

Encryption: Strong cryptographic tools like PGP (Pretty Good Privacy) enabled secure communication beyond government reach.

Decentralization: They rejected centralized authorities, believing that distributed networks prevented any single entity from wielding control.

The movement’s 1993 “Cypherpunk Manifesto” declared that electronic privacy was essential for open society. Their work—including anonymous remailers, digital cash experiments, and the ideological groundwork for Bitcoin—directly challenged mass surveillance and laid the foundation for today’s blockchain, cryptocurrency, and privacy-focused technologies.

Early Attempts at Digital Cash

David Chaum’s DigiCash (1989): Blind Signatures and Centralized Control

David Chaum’s DigiCash (1989) introduced blind signatures, allowing a bank to digitally sign currency without seeing it—preserving user privacy. However, it relied on centralized control: a single company maintained the ledger, verifying all transactions to prevent double-spending, creating a vulnerable point of failure and authority.

Adam Back’s Hashcash (1997): The Birth of Proof-of-Work (to fight spam)

Adam Back’s Hashcash (1997) introduced Proof-of-Work as a spam deterrent. Senders had to perform a small computational calculation—taking seconds—to generate a hash-based stamp. This made mass email spamming economically impractical due to cumulative computing costs, pioneering the mechanism later central to Bitcoin’s decentralized consensus and mining.

Wei Dai’s b-money (1998): A Proposal for Anonymous, Distributed Electronic Cash

Wei Dai’s b-money (1998) proposed the first anonymous, distributed digital cash system. It envisioned a network of nodes maintaining a collective ledger, using Proof-of-Work for currency creation and collective agreement for transaction validation. Though never implemented, b-money directly inspired Bitcoin, with Satoshi Nakamoto citing it as a foundational influence.

Nick Szabo’s Bit Gold (1998-2005): The Direct Predecessor to Bitcoin

Nick Szabo’s Bit Gold (1998–2005) directly prefigured Bitcoin. It proposed a decentralized digital currency where roof-of-Work generated cryptographic puzzle solutions, each becoming a new “bit gold” piece. These pieces formed a chain of ownership secured by timestamping. Szabo’s model solved double-spending without central authority, but lacked a practical implementation until Bitcoin emerged.

The Double-Spending Problem: Why a Central Authority Was Previously Considered Essential

The double-spending problem is unique to digital money : unlike physical cash, digital files are easily copied. Without safeguards, a user could spend the same digital coin multiple times before the system detects fraud.

Before Bitcoin, the only known solution was a central authority—like a bank or DigiCash—that maintained a master ledger. This intermediary verified every transaction, ensuring no coin was spent twice. Centralization was considered essential because no one had yet devised a way for untrusted, distributed parties to agree on transaction order without a single point of control.

The Dawn of a New Paradigm (2008-2012)

The Bitcoin Whitepaper & The Cypherpunk Manifesto Realized

October 31, 2008: The Release of the Bitcoin Whitepaper by Satoshi Nakamoto

On October 31, 2008, an anonymous individual or group using the pseudonym Satoshi Nakamoto published the Bitcoin whitepaper titled “Bitcoin: A Peer-to-Peer Electronic Cash System.” The paper proposed a revolutionary solution to the double-spending problem without requiring a central authority. By combining Proof-of-Work, a timestamp server, and a decentralized network of nodes maintaining a shared blockchain, Satoshi created a system where trust emerged from cryptographic proof rather than intermediaries. This marked the culmination of decades of Cypherpunk ideas—from Hashcash to Bit Gold—into a fully functional, decentralized digital currency that launched in January 2009.

Key Innovations Introduced

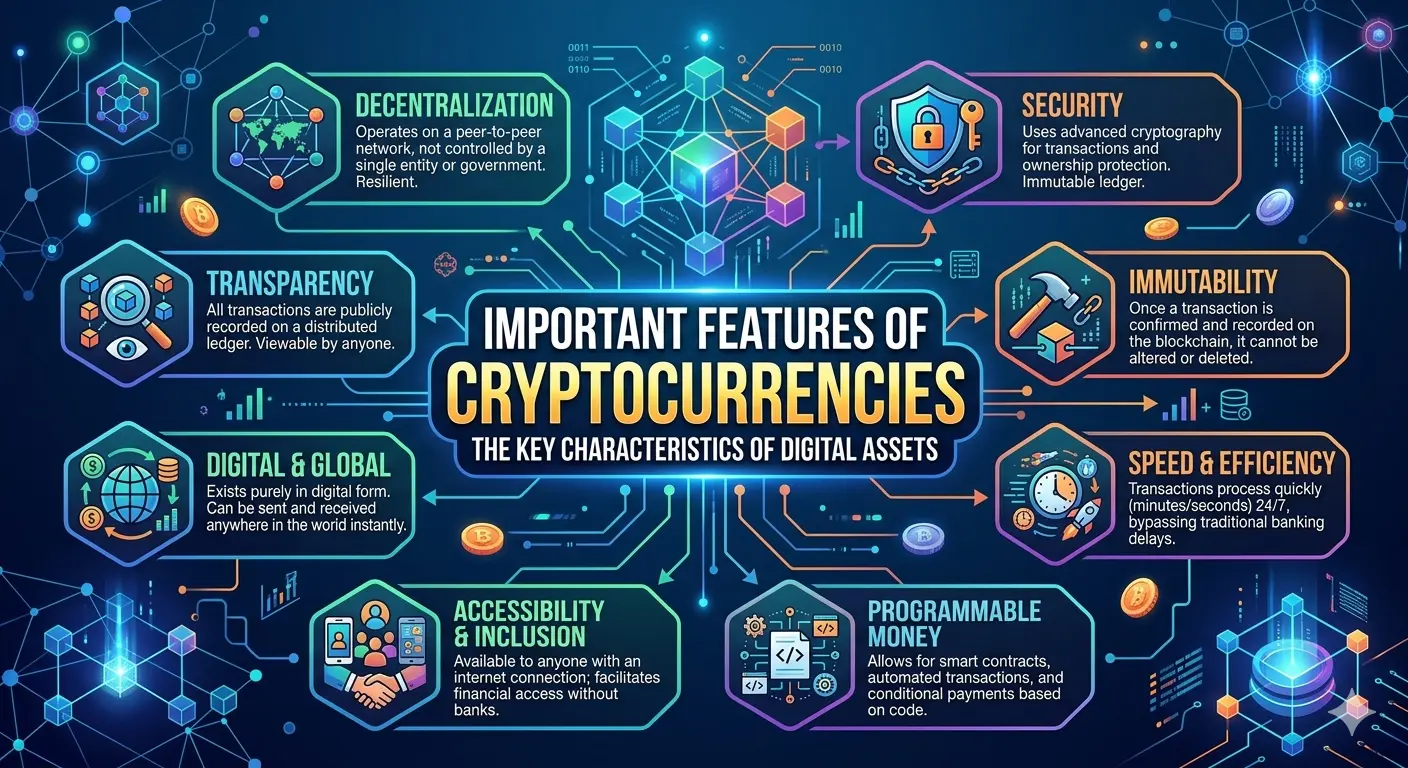

1.The Blockchain: A Distributed, Immutable Ledger

The blockchain is the foundational innovation behind Bitcoin—a distributed, immutable ledger that records transactions across a network of computers without any central authority. Unlike a traditional database controlled by a single entity, the blockchain is maintained collectively by thousands of nodes (participating computers) worldwide.

How it works:

Transactions are grouped into blocks. Each block contains a cryptographic hash of the previous block, creating an unbreakable chain. To add a new block, nodes compete to solve a complex Proof-of-Work puzzle—a process called mining. The first node to solve it broadcasts the block to the network, where other nodes verify its validity. Once confirmed, the block is permanently added, and the miner receives newly minted bitcoin as a reward.

Why it’s immutable:

Altering a single transaction would require re-mining that block and all subsequent blocks—a computationally impossible task if an attacker controls less than 50% of the network’s mining power. This makes the ledger tamper-evident and historically immutable.

Decentralization Trust

By distributing the ledger across thousands of independent nodes, the blockchain eliminates the need for a trusted intermediary. Trust is replaced by cryptographic verification and consensus. This design solved the double-spending problem, enabling peer-to-peer digital cash for the first time—all without banks, governments, or central authorities.

2.A Decentralized Consensus Mechanism: Solving Double-Spending Without a Central Authority

The decentralized consensus mechanism is the breakthrough that solved the double-spending problem without a central authority. In traditional systems, a bank maintains a single ledger to prevent fraud. Bitcoin replaced this trusted intermediary with a distributed network of nodes that collectively agree on the true state of transactions.

How consensus works:

Transactions are broadcast to the network and gathered into a candidate block by miners.

Miners compete to solve a Proof-of-Work puzzle—an energy-intensive computational task. The first miner to succeed broadcasts their valid block.

Other nodes verify the block’s transactions and Proof-of-Work. If valid, they add it to their copy of the blockchain.

The network converges on the longest valid chain, representing the collective agreement.

This Nakamoto Consensus ensures that all honest nodes maintain identical ledgers. An attacker would need overwhelming computational power (over 50% of the network’s mining capacity) to reverse transactions—a practically impossible and economically irrational act. Thus, cryptographic proof replaces institutional trust, enabling true peer-to-peer digital cash

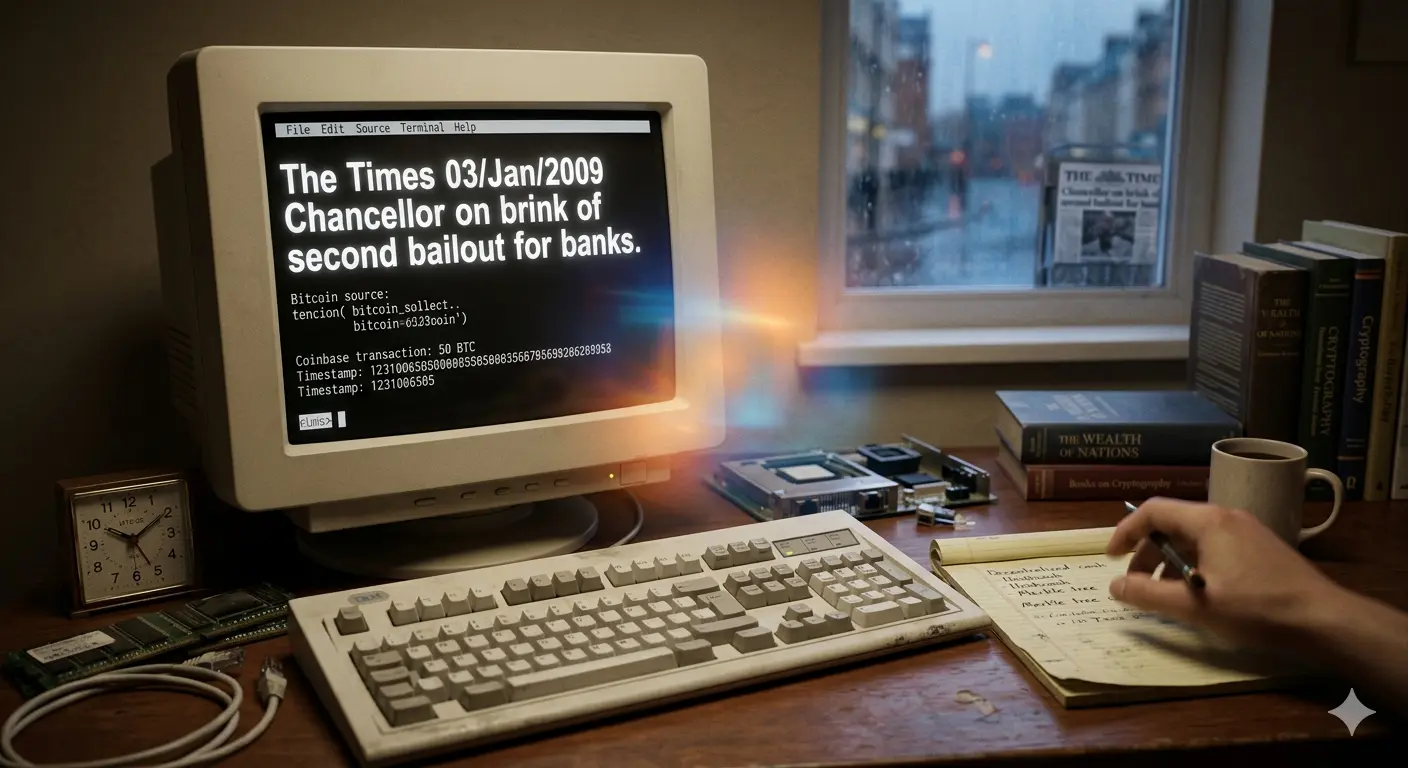

3.The Genesis Block: January 3, 2009, and the Embedded Message of Financial Instability

On January 3, 2009, Satoshi Nakamoto mined the Genesis Block (Block 0)—the first block of the Bitcoin blockchain. Embedded within its coinbase transaction was a conspicuous message:

“The Times 03/Jan/2009 Chancellor on brink of second bailout for banks.”

This headline from The Times newspaper was no coincidence. It referenced the British government’s imminent second bailout of struggling banks during the 2008 global financial crisis. Satoshi deliberately timestamped the message, serving multiple purposes:

Proof of launch: It established that no blocks were mined before this date.

Political statement: It highlighted the fragility of the traditional banking system—a system built on centralized control, bailouts, and inflationary monetary policy.

Philosophical anchor: The message underscored Bitcoin’s purpose: a decentralized alternative immune to institutional failure, where no single entity could print money or demand taxpayer-funded rescues.

The Genesis Block thus functioned as both technical foundation and ideological manifesto—encapsulating the Cypherpunk dream of financial sovereignty outside state and banking control from the very first moment of Bitcoin’s existence.

The Early Era: From Obscurity to First Transactions

The First "Miners" and the Initial Distribution

In Bitcoin’s earliest days, mining was radically different from today’s industrial-scale operations. After launching the network on January 9, 2009 (when the open-source software was released), Satoshi Nakamoto mined the first blocks alone, earning 50 BTC per block as a block reward. This initial phase involved only a handful of early adopters—cryptographers, cypherpunks, and hobbyists—running the software on ordinary personal computers with central processing units (CPUs) , long before specialized ASIC hardware existed.

The initial distribution was remarkably egalitarian by design. There was no pre-mine, no initial coin offering, and no privileged allocation to insiders. Anyone who downloaded the software and ran a node could participate equally. Hal Finney, a renowned cryptographer and cypherpunk, received the first-ever Bitcoin transaction from Satoshi on January 12, 2009—10 BTC sent as a test.

This ethos of open participation reflected the movement’s ideals: no central authority controlled issuance, and access was universal. Over time, as Bitcoin gained value, mining evolved into a specialized industry, but its foundational distribution remained a uniquely fair launch in financial history.

The First Real-World Transaction: May 22, 2010 (10,000 BTC for Two Papa John's Pizzas)

On May 22, 2010, programmer Laszlo Hanyecz made history by completing the first real-world Bitcoin transaction. He paid 10,000 BTC for two Papa John’s pizzas delivered to his home in Florida. At the time, Bitcoin had little monetary value—Laszlo had mined the coins when they were worth fractions of a penny. Today, that transaction is celebrated annually as Bitcoin Pizza Day. While those 10,000 BTC would later be worth hundreds of millions, the event demonstrated Bitcoin’s viability as actual currency, moving beyond theory into practical, peer-to-peer commerce.

The Emergence of the First Exchanges: From CPU Mining to GPU Mining

As Bitcoin gained value following the first pizza transaction, the need for liquidity and price discovery led to the emergence of the first exchanges. In 2010, BitcoinMarket.com launched, allowing users to trade BTC for fiat currency. These early platforms transformed Bitcoin from a hobbyist experiment into a tradable asset.

Simultaneously, mining underwent rapid evolution. Miners discovered that graphics processing units (GPUs) were far more efficient than CPUs for hashing calculations. By mid-2010, GPU mining rigs dominated, accelerating the network’s hash rate and intensifying competition. This shift marked the end of egalitarian CPU mining, as participants increasingly sought competitive advantages foreshadowing the specialized mining industry to come. Exchanges and advanced hardware together propelled Bitcoin toward greater mainstream attention.

The First Alternative Cryptocurrency ("Altcoin"): Namecoin (2011) and Litecoin (2011)

Following Bitcoin’s success, the first alternative cryptocurrencies emerged in 2011, expanding the blockchain landscape.

Namecoin (April 2011) was the first fork of Bitcoin. It introduced a decentralized naming system (like .bit domains), aiming to resist censorship by storing domain registrations on a blockchain—a novel application beyond currency.

Litecoin (October 2011), created by Charlie Lee, positioned itself as “silver to Bitcoin’s gold.” It offered technical modifications: faster block generation (2.5 minutes vs. 10), a different hashing algorithm (Scrypt), and a larger total supply. Litecoin demonstrated that blockchain protocols could be forked and optimized for different priorities—speed, accessibility, and fair mining with consumer-grade hardware.

These early altcoins proved that Bitcoin’s underlying technology was adaptable, sparking a wave of innovation that would ultimately lead to thousands of cryptocurrencies and the broader blockchain ecosystem.

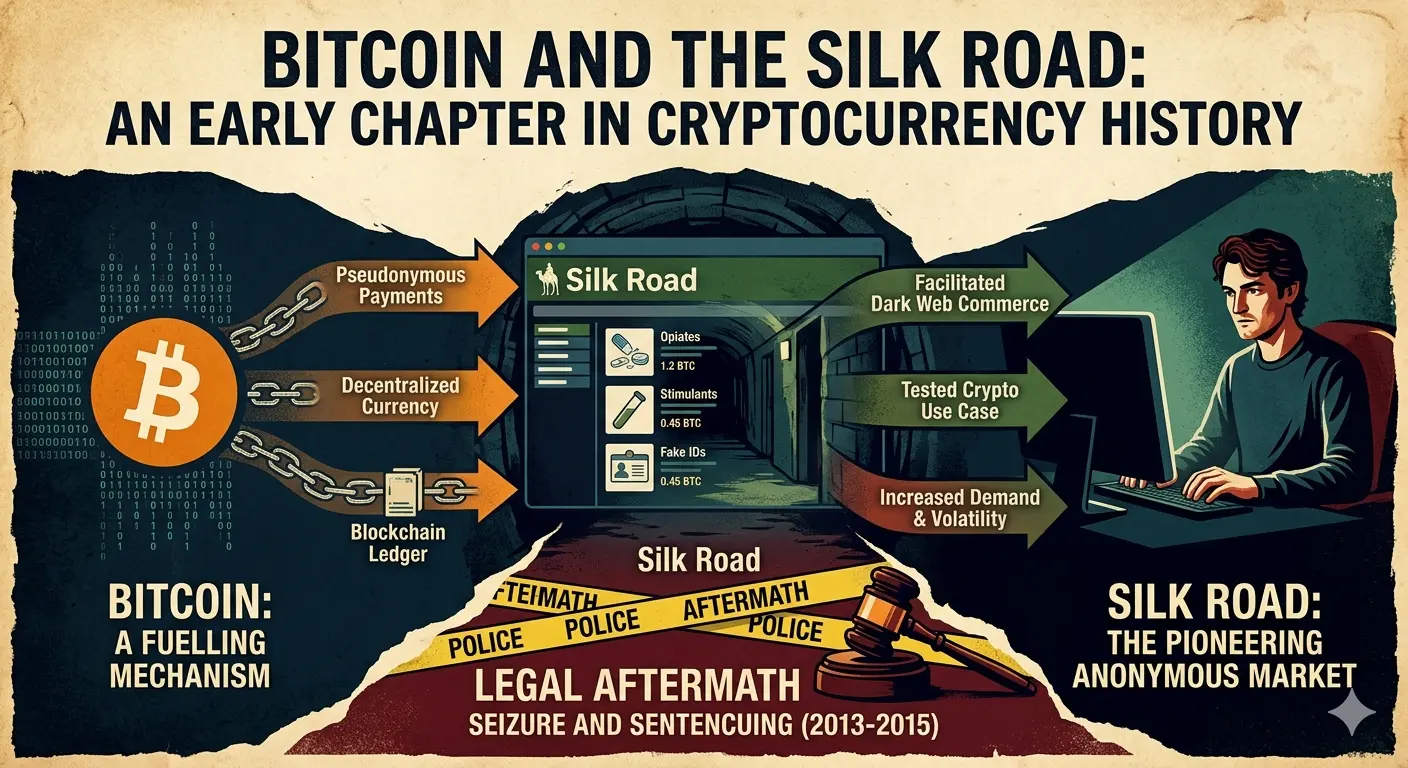

The Silk Road Era: Cryptocurrency's First Major Use Case (and Its Reputational Baggage)

From 2011 to 2013, the darknet marketplace Silk Road became cryptocurrency’s first major real-world use case. Founded by Ross Ulbricht (pseudonym “Dread Pirate Roberts”), Silk Road operated on the Tor network, allowing users to buy and sell illicit goods—primarily drugs—using Bitcoin’s pseudonymous transactions.

This association gave Bitcoin its reputational baggage. Media coverage often framed cryptocurrency as a tool for criminals, money launderers, and black-market commerce. Law enforcement agencies worldwide took notice, leading to the FBI’s 2013 takedown of Silk Road and Ulbricht’s subsequent life sentence.

However, the Silk Road era also provided unintended validation. It demonstrated Bitcoin’s functionality as genuine digital cash—resistant to seizure, borderless, and capable of facilitating voluntary exchange outside traditional financial systems. The infrastructure built around Silk Road (escrow systems, reputation mechanisms) foreshadowed decentralized finance concepts. Despite its notoriety, this period proved that censorship-resistant, peer-to-peer digital currency could work at scale, cementing Bitcoin’s practical viability beyond ideological circles.

Maturation, Expansion & Ideological Schisms (2013-2016)

The Rise of Altcoins & The First Market Cycles

The 2013 Bull Run: Bitcoin's First Major Price Peak

In 2013, Bitcoin experienced its first dramatic bull run, capturing global attention. The price surged from around $13 in January to a peak of over $1,100 in November—a staggering rise of nearly 8,000%. Several factors fueled this: growing media coverage, the Cyprus banking crisis (which drove interest in decentralized alternatives), increasing exchange accessibility, and speculative frenzy.

This bubble, however, was followed by a sharp crash, with prices falling below $200 by 2015. Despite the volatility, the 2013 rally established Bitcoin as a volatile but persistent asset class, attracting investors, entrepreneurs, and regulators who could no longer ignore the emerging cryptocurrency phenomenon.

The Mt. Gox Collapse (2014): A Defining Crisis of Centralized Custody

In February 2014, Mt. Gox—once handling over 70% of global Bitcoin transactions—collapsed spectacularly. The Tokyo-based exchange filed for bankruptcy, claiming it had lost approximately 850,000 BTC (worth $450 million at the time) due to years of poor security, hacking, and mismanagement.

The crisis became a defining lesson in centralized custody risks. Users who stored funds on the exchange lost everything, directly contradicting Bitcoin’s promise of self-sovereignty. The debacle underscored the cypherpunk mantra: “Not your keys, not your coins.” It accelerated development of secure wallets, multisignature technology, and decentralized exchanges, pushing the ecosystem toward greater user control and hardening the industry against future failures.

The Ideological Split: The "Blocksize Wars" and the Birth of Bitcoin Cash (BCH)

Between 2015 and 2017, Bitcoin faced an intense ideological and technical conflict known as the Blocksize Wars. One faction sought to scale Bitcoin by increasing the block size limit for more on-chain transactions. The opposing faction favored maintaining smaller blocks (1MB) while developing second-layer solutions like the Lightning Network for scalability, prioritizing decentralization over throughput.

The dispute culminated in August 2017, when a hard fork created Bitcoin Cash (BCH) —a new cryptocurrency with larger 8MB blocks. This schism reflected deeper philosophical tensions: whether Bitcoin should evolve into a global settlement layer or remain a peer-to-peer electronic cash system, as originally described in Satoshi’s whitepaper.

The Altcoin Explosion

Litecoin (LTC): “The Silver to Bitcoin’s Gold”

Created by Charlie Lee in 2011, Litecoin was designed as a lighter, faster alternative to Bitcoin. It features 2.5-minute block times (vs. 10 minutes), uses the Scrypt hashing algorithm for ASIC-resistant mining, and has a total supply of 84 million coins—four times Bitcoin’s cap.

Ripple (XRP): Targeting the Interbank Settlement System

Ripple (XRP) , launched in 2012, targets the interbank settlement system. Unlike decentralized cryptocurrencies, Ripple uses a consensus ledger with trusted validators to enable fast, low-cost cross-border payments for financial institutions. It prioritizes enterprise adoption over decentralization, positioning itself as a bridge currency for traditional banking infrastructure.

Dogecoin (DOGE): The First “Meme Coin” and Its Cultural Impact

Launched in 2013 as a joke by Billy Markus and Jackson Palmer, Dogecoin featured the Shiba Inu “Doge” meme. Despite its satirical origins, it developed a passionate community known for tipping, charity fundraising, and later, high-profile endorsements. It became the first meme coin, demonstrating crypto’s cultural and speculative dimensions.

The Introduction of Programmability: Ethereum

The Vision of Vitalik Buterin: Bitcoin's Limitations and the Need for a World Computer

Vitalik Buterin, a programmer and Bitcoin Magazine co-founder, recognized Bitcoin’s limitations: its scripting language was intentionally restricted for security, preventing complex applications beyond simple transactions. He envisioned a “world computer” —a decentralized platform where developers could build any application using smart contracts, self-executing code running on a blockchain.

This vision addressed the gap between Bitcoin as digital gold and the broader potential of decentralized technology. Buterin formally proposed Ethereum in late 2013, arguing that a Turing-complete blockchain could power everything from decentralized finance to autonomous organizations, expanding cryptocurrency from currency into a general-purpose decentralized computing platform.

Ethereum’s Whitepaper (2013) and Launch (2015)

Vitalik Buterin published the Ethereum whitepaper in late 2013, proposing a blockchain with Turing-complete scripting—enabling developers to deploy smart contracts beyond simple transactions. Following a crowdsale in 2014 that raised over $18 million (the first major initial coin offering), the Ethereum network launched on July 30, 2015.

The genesis block, “Frontier,” marked the beginning of a platform designed as a decentralized world computer. Unlike Bitcoin’s limited scripting, Ethereum allowed programmable applications—decentralized applications (dApps) —to run exactly as coded, without censorship, downtime, or third-party interference, fundamentally expanding blockchain’s potential beyond digital currency.

Smart Contracts: Self-Executing Agreements on the Blockchain

A smart contract is a self-executing program stored on a blockchain that automatically enforces the terms of an agreement when predetermined conditions are met. Unlike traditional contracts requiring intermediaries like lawyers or courts, smart contracts run exactly as coded—immutable, transparent, and trustless.

On Ethereum, developers write smart contracts in languages like Solidity. Once deployed, the contract resides on the blockchain, and anyone can interact with it. Use cases include decentralized finance (lending without banks), automated escrow, and token creation. Smart contracts transform blockchain from a simple ledger into a programmable platform, enabling complex decentralized applications without relying on centralized intermediaries.

he ERC-20 Token Standard: The Foundation for a New Economy

The ERC-20 token standard, proposed by Fabian Vogelsteller in late 2015, established a common set of rules for creating fungible tokens on Ethereum. Before ERC-20, each new token required custom code, creating fragmentation and exchange difficulties. The standard defined basic functions—transferring balances, approving allowances, and querying totals—ensuring seamless compatibility across wallets, exchanges, and decentralized applications.

This standardization unleashed the token economy. Thousands of projects launched their own ERC-20 tokens through Initial Coin Offerings (ICOs), democratizing fundraising but also inviting speculation and scams. ERC-20 became the foundation for decentralized finance (DeFi), governance tokens, and the broader ecosystem, cementing Ethereum’s role as the primary platform for digital assets.

The DAO (Decentralized Autonomous Organization) Incident (2016)

The $60 Million Hack

The $60 million hack refers to the 2016 DAO (Decentralized Autonomous Organization) attack, one of Ethereum’s most defining crises. A vulnerability in the DAO’s smart contract allowed an attacker to drain approximately 3.6 million ETH (worth $60 million at the time). The event sparked an existential debate: should Ethereum hard fork to reverse the theft, violating immutability, or accept the loss? The community controversially chose to fork, creating Ethereum (ETH) and the original chain Ethereum Classic (ETC) , splitting the ecosystem permanently.

The Contentious Hard Fork: Ethereum (ETH) vs. Ethereum Classic (ETC)

The 2016 DAO hack forced Ethereum into a philosophical split. The majority supported a hard fork to reverse the stolen funds, prioritizing restitution over strict immutability—creating Ethereum (ETH) . A minority rejected this as a violation of “code is law,” continuing the original, unaltered chain as Ethereum Classic (ETC) . This division crystallized a foundational tension in blockchain governance: adaptability versus absolute immutability.

The ICO Boom & The Age of Experimentation (2017-2019)

The Tokenization of Everything

The Initial Coin Offering (ICO) Mania of 2017-2018

Between 2017 and 2018, the Initial Coin Offering (ICO) boom transformed cryptocurrency fundraising. Leveraging Ethereum’s ERC-20 token standard, startups raised billions by selling custom tokens directly to the public—bypassing traditional venture capital. At its peak, ICOs raised over $6 billion in 2017, with projects like Filecoin and Tezos amassing hundreds of millions.

This speculative frenzy attracted innovators, fraudsters, and regulators alike. While funding countless blockchain experiments, the mania also produced numerous scams and unsustainable projects, culminating in a market crash. The ICO era democratized capital formation but ultimately invited intense regulatory scrutiny, reshaping how crypto projects raise funds.

How ICOs Worked: Whitepapers, Utility Tokens, and Unregulated Fundraisin

Initial Coin Offerings (ICOs) allowed blockchain projects to raise capital by issuing utility tokens directly to the public, typically on Ethereum using the ERC-20 standard. A project published a whitepaper outlining its vision, technology, and token economics. Investors sent cryptocurrency (mostly Bitcoin or Ethereum) to a smart contract address and received newly minted tokens in return.

These tokens promised future access to a product or service—not equity or ownership. Operating in a largely unregulated environment, ICOs bypassed traditional securities laws, enabling rapid, global fundraising. While this democratized access to early-stage investment, it also attracted scams, insufficient due diligence, and regulatory backlash that ultimately reshaped token issuance through securities enforcement.

The 2017 Bull Run: Bitcoin's Historic Ascent to $20,000

In 2017, Bitcoin experienced its most dramatic bull run to date, surging from around $1,000 in January to an all-time high of nearly $20,000 in December. Fueled by retail mania, media frenzy, and the ICO boom (which drove demand for ETH and BTC as entry currencies), the rally captured global attention. Mainstream platforms like CME Group launched Bitcoin futures, signaling institutional curiosity.

The bubble burst shortly after, with prices falling below $6,000 by early 2018. Despite the crash, 2017 cemented Bitcoin’s cultural and financial presence, attracting a wave of retail investors, sparking regulatory debates, and establishing cryptocurrency as a volatile yet enduring asset class.

The Great "Crypto Winter" of 2018: The Bursting of the Speculative Bubble

Following the 2017 peak, 2018 marked the onset of the “Crypto Winter” —a prolonged bear market where Bitcoin plummeted from nearly $20,000 to around $3,100 by December, a decline of over 80%. The collapse mirrored the bursting of the ICO bubble, with countless projects folding as speculative capital evaporated.

This period, however, was crucial for maturation. Overleveraged speculators exited; legitimate builders remained. Development continued on infrastructure, scaling solutions like the Lightning Network, and foundational protocols. Regulatory clarity began emerging globally. Crypto Winter served as a necessary “cleansing” cycle, shifting focus from hype to sustainable innovation, laying groundwork for the institutional interest that would return in subsequent years.

Infrastructure & Scaling Solutions

The Scaling Debate Revisited: Layer 1 vs. Layer 2 Solutions

The scaling debate centers on how blockchains can handle more transactions without sacrificing decentralization. Layer 1 solutions modify the base protocol—increasing block size (Bitcoin Cash) or sharding (Ethereum 2.0)—to process more on-chain. Layer 2 solutions build atop existing chains, handling transactions off-chain while settling finality on the main chain.

Key Layer 2 examples include Bitcoin’s Lightning Network (fast, low-cost micropayments) and Ethereum’s rollups (bundling transactions off-chain with cryptographic proofs). The debate reflects philosophical tensions: Layer 1 prioritizes base-layer capacity, while Layer 2 emphasizes preserving decentralization while achieving scalability—an ongoing evolution rather than a settled solution.

Bitcoin's Scaling Path: The SegWit Upgrade and the Lightning Network (Fast, Off-Chain Transactions)

Bitcoin’s scaling strategy evolved through two key developments: Segregated Witness (SegWit) and the Lightning Network.

Activated in August 2017, SegWit restructured transaction data, effectively increasing block capacity without altering the 1MB limit by separating signature data. This fixed transaction malleability, enabling Layer 2 solutions.

The Lightning Network is a second-layer protocol enabling fast, low-cost, off-chain transactions. Users open payment channels, conduct unlimited transactions instantly, then settle final balances on-chain. This allows Bitcoin to handle millions of microtransactions—coffee purchases, streaming payments—without congesting the base layer, preserving decentralization while achieving scalable, everyday usability.

Ethereum's Scaling Path: The Roadmap Toward Sharding and Layer 2 (Plasma, Rollups)

Ethereum’s scaling roadmap balances Layer 1 improvements with Layer 2 adoption.

Sharding, central to Ethereum 2.0, splits the blockchain into parallel “shards,” distributing transaction processing across the network to increase throughput dramatically.

Complementing this, Layer 2 solutions like Plasma (child chains with fraud proofs) and rollups (bundling off-chain transactions with proofs settled on Ethereum) provide immediate scalability. Optimistic rollups assume validity unless challenged; ZK-rollups use cryptographic validity proofs.

Together, these approaches aim to achieve “The Surge” —scaling Ethereum to handle thousands of transactions per second while maintaining decentralization, security, and composability across the ecosystem.

The Rise of New Layer-1 Blockchains: Cardano, Solana, Polkadot, and Avalanche

As Ethereum faced scaling challenges, new Layer-1 blockchains emerged, each offering distinct technical approaches. Cardano (2017) emphasized peer-reviewed research and formal methods. Solana (2020) pursued high throughput through its novel Proof-of-History consensus, processing thousands of transactions per second. Polkadot (2020), founded by Ethereum co-founder Gavin Wood, introduced a multi-chain architecture enabling specialized parachains to interoperate. Avalanche (2020) offered sub-second finality and customizable subnets.

These platforms competed for developers and liquidity, sparking the “L1 wars.” While expanding blockchain diversity, they also fragmented liquidity and user bases, fueling debates about optimal scalability, decentralization trade-offs, and the future of multi-chain ecosystems.

Institutionalization & Mainstream Adoption (2020-2023)

DeFi: Rebuilding Finance Without Intermediaries

Decentralized Finance (DeFi) Summer (2020)

The DeFi Summer of 2020 marked an explosion of decentralized financial applications on Ethereum, transforming it from a speculative platform into a functional parallel financial system. Catalyzed by innovations like automated market makers (Uniswap) , lending protocols (Aave, Compound) , and yield farming (incentivizing liquidity with token rewards), total value locked (TVL) in DeFi surged from under $1 billion to over $10 billion within months.

This period demonstrated that complex financial activities—trading, lending, borrowing—could operate without banks or intermediaries, governed entirely by smart contracts. DeFi Summer established decentralized finance as a core crypto use case, attracting developers, capital, and regulatory scrutiny.

Key DeFi Primitives:

Decentralized Exchanges (DEXs): Uniswap and Automated Market Makers (AMMs)

Decentralized exchanges (DEXs) allow peer-to-peer cryptocurrency trading without intermediaries. Unlike centralized exchanges (e.g., Coinbase), DEXs let users retain custody of their funds, executing trades via smart contracts.

Uniswap, launched in 2018, pioneered the automated market maker (AMM) model. Instead of traditional order books, Uniswap uses liquidity pools—users deposit token pairs into pools and earn trading fees. Prices are algorithmically determined by a constant product formula (x y = k).

This innovation democratized market making: anyone could provide liquidity and earn passive yield. AMMs became the backbone of DeFi, enabling permissionless, always-on trading, and inspiring countless forks and innovations across blockchain ecosystems.

Lending & Borrowing Protocols: Aave and Compound

Aave and Compound are foundational lending and borrowing protocols in decentralized finance (DeFi), enabling users to earn interest on deposits or take out loans without traditional intermediaries.

Compound (launched 2018) pioneered algorithmic money markets—users supply assets to liquidity pools, earning variable interest rates determined algorithmically by supply and demand. Borrowers provide collateral (overcollateralized) to secure loans.

Aave (launched 2020) expanded on this with features like flash loans (uncollateralized loans repaid within a single transaction), interest rate switching, and multiple collateral types.

Together, these protocols replaced banks with smart contracts, creating a transparent, permissionless credit market accessible globally, 24/7. They became cornerstones of the DeFi ecosystem.

Yield Farming and Liquidity Mining

Yield farming (or liquidity mining) is the practice of earning rewards by providing liquidity to DeFi protocols. Users deposit assets into protocols—such as lending markets or decentralized exchanges—and receive governance tokens in addition to trading fees or interest.

The 2020 DeFi Summer popularized this model: protocols like Compound distributed COMP tokens to lenders and borrowers, sparking a “farm frenzy.” Yield farmers aggressively moved capital between protocols chasing highest returns, sometimes leveraging, compounding, and automating strategies.

While this bootstrapped liquidity and decentralized governance, it also introduced risks: impermanent loss, smart contract vulnerabilities, and high gas fees. Yield farming transformed DeFi into a highly competitive, capital-efficient ecosystem.

The "Liquidity Crisis" and DeFi Hacks: A Maturing but Risky Sector

As DeFi exploded in 2020-2021, the sector faced recurring liquidity crises and high-profile hacks, revealing the risks of unaudited, composable smart contracts.

Liquidity crises emerged when protocols offered unsustainable token incentives. When rewards diminished or market sentiment shifted, liquidity fled rapidly, causing cascading liquidations and protocol insolvencies—most notably during the 2020 “Black Thursday” crash, where MakerDAO saw mass liquidations due to Ethereum network congestion.

Simultaneously, DeFi hacks exposed vulnerabilities in unaudited code, oracle manipulation, and complex interdependencies. Major exploits included the bZx flash loan attacks (2020), Compound’s distribution bug (2021), and millions lost in cross-chain bridge hacks. These events demonstrated that DeFi’s composability—“money legos”—could amplify systemic risk.

Despite these setbacks, each incident forced protocol maturation: improved oracle systems (Chainlink), rigorous audits, formal verification, and insurance protocols emerged. DeFi evolved from speculative experimentation into a sector increasingly focused on security, sustainability, and risk management—though risks remain inherent to permissionless, rapidly innovating environments.

NFTs: Digital Ownership & The Creator Economy

Non-Fungible Tokens (NFTs): From CryptoKitties (2017) to the 2021 Explosion

Non-Fungible Tokens (NFTs) are unique digital assets verified on a blockchain, representing ownership of art, collectibles, gaming items, or virtual real estate. Unlike fungible cryptocurrencies (like Bitcoin or Ether), each NFT is distinct and cannot be exchanged on a one-to-one basis.

The NFT phenomenon began with CryptoKitties in late 2017, a game where users bred and traded unique digital cats. The project became so popular it congested the Ethereum network, demonstrating demand for digital ownership. However, the NFT market remained niche until 2021, when it exploded into mainstream consciousness.

The 2021 boom was fueled by several factors: high-profile sales like Beeple’s “Everydays” selling for $69 million at Christie’s; the rise of profile picture (PFP) projects such as Bored Ape Yacht Club and CryptoPunks, which became status symbols; and integration with gaming, music, and virtual worlds (the metaverse). Celebrities, brands, and traditional art institutions rushed in, pushing total NFT trading volume to over $25 billion that year.

Critics decried speculation, environmental concerns (prior to Ethereum’s proof-of-stake transition), and rampant scams. Yet NFTs fundamentally shifted digital ownership, enabling creators to monetize work via royalties and fostering communities around shared digital assets, cementing their place in crypto culture.

The Concept of Provenance, Scarcity, and Digital Art

NFTs introduced three transformative concepts to the digital realm: provenance, scarcity, and verifiable ownership.

Provenance is an immutable record of ownership history stored on the blockchain. For digital art, this solves a long-standing problem: unlike physical art, digital files can be copied infinitely with no original. An NFT establishes a cryptographically verifiable chain of custody—from creator to current owner—providing authenticity previously impossible in digital media.

Scarcity is programmatically enforced. Creators can mint limited editions or single unique works, with the blockchain ensuring no unauthorized additional copies can be created. This digital scarcity mimics physical art markets, creating value through limited supply.

For digital art, NFTs offered artists a sustainable model: direct-to-fan sales without galleries, and crucially, programmable royalties—automatic payments to creators each time the work resells on secondary markets. This transformed digital creation from an unbuyable medium into an asset class, empowering artists with ongoing revenue streams while collectors gained verifiable ownership of culturally significant digital artifacts.

Major NFT Marketplaces: OpenSea and the Royalty Debate

OpenSea, launched in 2017, became the dominant NFT marketplace, handling billions in trading volume by 2021-2022. It functioned as a decentralized eBay for digital assets, enabling creators to mint, list, and trade NFTs across multiple blockchains.

A central controversy emerged around creator royalties—automatic secondary-market fees (typically 5-10%) coded into NFTs to sustain artists beyond initial sales. In 2022, OpenSea and competitors like Blur began reducing or eliminating mandatory royalties, sparking intense backlash. Proponents argued lower fees improved liquidity; critics contended this undermined the economic promise that attracted creators to NFTs.

The royalty debate exposed tensions between platform profitability, trader incentives, and creator sustainability. It forced the ecosystem to explore alternatives: royalty-enforcing smart contracts, community-driven enforcement, and decentralized marketplaces prioritizing creator compensation over trading volume.

NFT Use Cases: Gaming, Collectibles, Real-World Asset Tokenization, and Identity

NFTs have expanded far beyond digital art, enabling diverse applications across industries:

Gaming: NFTs represent true ownership of in-game assets—skins, weapons, virtual land—allowing players to trade or sell items across marketplaces. Games like Axie Infinity pioneered “play-to-earn,” where players earned income through NFT-based gameplay, while virtual worlds like The Sandbox and Decentraland use NFTs for land ownership and user-generated content, creating player-driven economies.

Collectibles: Profile picture (PFP) projects like CryptoPunks and Bored Ape Yacht Club became cultural status symbols, with communities forming around exclusive membership perks, events, and IP commercialization. Sports collectibles platforms like NBA Top Shot introduced mainstream audiences to NFT-based trading cards.

Real-World Asset (RWA) Tokenization: NFTs can represent fractional or full ownership of physical assets—real estate, art, luxury goods—on blockchain. This enables fractional investment, increased liquidity, and transparent ownership records. Projects now tokenize everything from wine collections to fine art, bridging traditional and digital finance.

Identity & Credentials: NFTs serve as self-sovereign identity tools. “Soulbound” tokens (non-transferable NFTs) represent academic credentials, professional certifications, or membership status. This allows individuals to control their identity without relying on centralized institutions. Decentralized identifiers (DIDs) and verifiable credentials built on NFT infrastructure offer tamper-proof, portable identity systems.

Additional use cases include ticketing (scalper-resistant event tickets), supply chain tracking (provenance of goods), and intellectual property management (automated royalty distribution). As the technology matures, NFTs increasingly function as foundational infrastructure for digital ownership, enabling verifiable scarcity, programmability, and user-controlled assets across virtually any domain where proof of authenticity, ownership, or access matters. The evolution continues toward interoperability, standardization, and integration with physical-world applications.

The Great Power Shift: Institutional Capital & Regulation

Corporate Adoption: Tesla, MicroStrategy, and Bitcoin on Balance Sheets

Beginning in 2020-2021, a wave of corporate adoption transformed Bitcoin from a niche internet asset into a mainstream treasury reserve asset, legitimizing cryptocurrency in traditional finance.

MicroStrategy, led by CEO Michael Saylor, pioneered this trend. Starting in August 2020, the business intelligence firm began accumulating Bitcoin as its primary treasury reserve asset, arguing it was a superior store of value to cash depreciating via inflation. As of today, MicroStrategy holds over 200,000 BTC, becoming effectively a Bitcoin proxy company and inspiring other corporations to follow.

Tesla, under CEO Elon Musk, made a landmark move in February 2021, announcing a $1.5 billion Bitcoin purchase and briefly accepting BTC as payment for vehicles (suspended later citing environmental concerns). This endorsement from the world’s most valuable automaker signaled mainstream corporate acceptance.

Other public companies—Square (now Block) , Coinbase, and numerous smaller firms—added Bitcoin to their balance sheets. This trend carried significant implications: it introduced Bitcoin to institutional investors, pressured accounting standards boards to develop crypto-specific guidelines, and validated Bitcoin’s role as “digital gold” within diversified corporate treasuries. Critics argued it concentrated risk and distracted from core business operations. Nevertheless, corporate adoption represented a pivotal shift: Bitcoin was no longer merely speculative retail asset but a recognized component of sophisticated corporate financial strategy, bridging cryptocurrency with traditional capital markets.

The Rise of Institutional Custody: Fidelity, BlackRock, and the Bitcoin Spot ETF

The maturation of cryptocurrency markets witnessed institutional custody solutions emerge as traditional finance giants recognized client demand for regulated crypto exposure.

Fidelity Investments launched Fidelity Digital Assets in 2018, offering institutional-grade custody and trade execution. As one of the world’s largest asset managers, Fidelity’s entry signaled legitimacy, providing secure, insured storage for pension funds, endowments, and family offices.

The watershed moment arrived with BlackRock, the world’s largest asset manager ($10+ trillion AUM). CEO Larry Fink shifted from Bitcoin skeptic to advocate, and BlackRock filed for a Bitcoin spot ETF in June 2023. After years of regulatory rejections, the SEC approved multiple spot Bitcoin ETFs in January 2024, including BlackRock’s iShares Bitcoin Trust (IBIT) and Fidelity’s Wise Origin Bitcoin Fund (FBTC).

This approval unlocked unprecedented institutional capital, simplifying Bitcoin investment through traditional brokerage accounts. Spot ETFs offered regulated, liquid, and familiar vehicles for advisors, pension funds, and retail investors, triggering billions in inflows and fundamentally reshaping Bitcoin’s market structure toward institutional permanence.

The Regulatory Crackdown:

The SEC vs. Ripple (XRP) Lawsuit

In December 2020, the SEC filed a lawsuit against Ripple Labs, alleging that XRP was an unregistered security and that Ripple executives had illegally raised $1.3 billion. The case became a landmark legal battle defining cryptocurrency classification.

In July 2023, Judge Analisa Torres delivered a split ruling: XRP sales on public exchanges were not securities (benefiting retail investors), but direct sales to institutions were securities (violating registration laws). This partial victory created legal nuance, influencing other SEC cases and providing clarity that tokens themselves are not inherently securities—context matters. The SEC’s appeal continues, keeping the industry watching.

The Collapse of Major Intermediaries: Terra/Luna (2022) and FTX (2022)

2022 witnessed the collapse of two major crypto intermediaries, triggering a systemic crisis and erasing billions in value.

Terra/Luna (May 2022) : The algorithmic stablecoin UST lost its peg, causing a death spiral that wiped out $40 billion virtually overnight. This exposed the fragility of unbacked, governance-dependent mechanisms.

FTX (November 2022) : Sam Bankman-Fried’s exchange collapsed due to commingling customer funds with its trading arm, Alameda Research. The fraud resulted in $8 billion in customer losses, criminal convictions, and severe reputational damage to centralized crypto entities. Together, these events reinforced the cypherpunk ethos: “not your keys, not your coins” and distrust of centralized custodians.

he Global Push for Clarity: MiCA in the European Union

The European Union’s Markets in Crypto-Assets (MiCA) regulation, finalized in 2023, established the world’s first comprehensive framework for digital assets. It creates uniform rules across 27 member states governing crypto-asset issuers, exchanges, and stablecoins, requiring licensing, consumer safeguards, capital reserves, and anti-money laundering compliance.

MiCA aims to balance innovation with investor protection while preventing another FTX-style collapse. Stablecoin issuers must maintain strict reserves. Implementation began in 2024, positioning the EU as a regulatory pioneer. This clarity has attracted crypto businesses seeking legal certainty, potentially serving as a model for global regulatory approaches.

The Current Era & Future Horizons (2024-Present & Beyond)

The Next Frontier: Scalability, Interoperability, & User Experience

Ethereum's "The Merge": The Transition from Proof-of-Work to Proof-of-Stake (2022)

On September 15, 2022, Ethereum executed “The Merge” —one of blockchain history’s most significant technical upgrades. The network transitioned from Proof-of-Work (PoW) to Proof-of-Stake (PoS), replacing energy-intensive mining with validators staking 32 ETH.

This shift delivered three transformative benefits:

1. Energy Reduction: Ethereum’s energy consumption dropped by ~99.9% , eliminating criticism about environmental impact.

2. Reduced Issuance: New ETH issuance fell by ~90%, creating a deflationary dynamic during network activity.

3. Scalability Foundation: The Merge laid groundwork for future scaling upgrades (sharding, rollups).

The transition occurred seamlessly with no network downtime—a testament to years of rigorous testing. While critics noted PoS introduced different centralization risks (validator concentration), The Merge positioned Ethereum as a sustainable, institution-friendly blockchain, crucial for long-term adoption. It represented the culmination of the “Ethereum 2.0” vision first proposed in 2013, fundamentally re-architecting the world’s largest smart contract platform.

The Dominance of Layer-2 Networks: Arbitrum, Optimism, and ZK-Rollups

Following Ethereum’s transition to Proof-of-Stake, Layer-2 (L2) networks emerged as the primary solution for scalability, offering fast, low-cost transactions while inheriting Ethereum’s security. By 2023-2024, L2s processed significantly more transactions than Ethereum’s mainnet, cementing their role as the network’s execution layer.

Arbitrum and Optimism, both optimistic rollups, dominate the L2 landscape. These networks assume transactions are valid unless challenged, posting compressed data to Ethereum. They offer an ecosystem of decentralized applications (dApps), bridging, and native governance tokens. Arbitrum leads in total value locked (TVL), while Optimism’s “Superchain” vision emphasizes interoperability across multiple chains.

ZK-rollups (zero-knowledge rollups) represent a competing paradigm: they generate cryptographic proofs (validity proofs) that batch transactions, settling finality on Ethereum without fraud game periods. zkSync Era, Polygon zkEVM, and Scroll lead this category. While technically complex, ZK-rollups offer faster withdrawals and stronger security assumptions than optimistic counterparts.

This L2 expansion has fragmented liquidity and user experience but drives massive scalability—handling thousands of transactions per second at fractions of a cent. The proliferation of L2-specific ecosystems and cross-chain interoperability protocols (LayerZero, Wormhole) reflects a modular blockchain future. Ethereum’s roadmap now envisions “The Surge”—making L2s capable of processing millions of transactions while maintaining decentralization, with L2s becoming the default user-facing layer for mainstream adoption.

Account Abstraction: Making Crypto User-Friendly (Seed Phrases vs. Social Recovery)

Account Abstraction, implemented via Ethereum’s ERC-4337 standard (2023), transforms crypto wallets from externally owned accounts (EOAs) into smart contract accounts, enabling programmable features that dramatically improve user experience.

The traditional model relies on seed phrases—12 or 24 words serving as master keys. This creates friction: users must store phrases securely offline; loss means permanent fund loss. This single point of failure has hindered mainstream adoption.

Account abstraction introduces social recovery: users designate trusted guardians (friends, institutions, hardware wallets) who can collectively restore access without seed phrases. Additional features include spending limits (allow transactions without unlimited approvals), automatic payments (subscriptions), and two-factor authentication on-chain.

By abstracting complex cryptographic operations, this upgrade makes crypto wallets behave more like familiar banking apps, removing critical barriers to mass adoption while maintaining self-custody principles.

The Intersection of Crypto & AI

Decentralized Compute Networks for AI Training

Decentralized compute networks aim to democratize artificial intelligence (AI) training by aggregating underutilized GPU resources globally, challenging centralized providers like Nvidia and cloud monopolies.

Projects such as Render Network, Akash Network, and Golem enable users to contribute idle computing power in exchange for tokens, while AI developers access lower-cost, distributed infrastructure for model training and inference. Blockchain ensures transparent pricing, verifiable execution, and payment settlement.

This intersection of crypto and AI addresses pressing concerns: centralized AI control, compute monopolies, and high barriers to entry. Decentralized compute promises more equitable access, censorship resistance, and alignment with open-source AI development, representing a growing frontier merging two transformative technologies.

. AI Agents Managing Crypto Wallets and DeFi Strategies

AI agents capable of managing crypto wallets and executing DeFi strategies represent an emerging frontier where artificial intelligence meets autonomous finance. These agents—powered by large language models and smart contract automation—can execute trades, provide liquidity, arbitrage across decentralized exchanges, and optimize yield farming strategies without human intervention.

Projects like Autonomous, Wayfinder, and various “intent-based” protocols enable users to set high-level goals (“earn 5% yield on USDC”), with AI agents determining optimal execution across lending protocols, DEXs, and layer-2 networks. This abstraction significantly lowers user expertise barriers.

However, risks include smart contract vulnerabilities, governance exploits, and the challenge of aligning AI objectives with user interests. As these systems mature, they may transform DeFi from manual, high-skill participation into accessible, automated wealth management—potentially onboarding mainstream users while raising questions about autonomy, security, and financial control.

Verifiable Data Provenance for AI Training Data via Blockchain

Verifiable data provenance uses blockchain to address critical challenges in AI development: training data authenticity, bias, consent, and compensation. By recording datasets on-chain, developers can cryptographically verify origin, ownership, and usage terms.

Projects like Ocean Protocol, Bagel, and Space and Time enable data creators to track how their contributions are used in AI models, ensure proper attribution, and receive automated micropayments via smart contracts. This transparency helps prevent unauthorized scraping, reduces bias through auditable datasets, and creates ethical, consent-based data economies.

As AI regulation intensifies, blockchain-based provenance offers technical solutions to emerging legal requirements for training data transparency and creator compensation.

Central Bank Digital Currencies (CBDCs) vs. Decentralized Crypto

What are CBDCs? The State-Sponsored Alternative

Central Bank Digital Currencies (CBDCs) are digital forms of fiat money issued and controlled by a nation’s central bank. Unlike decentralized cryptocurrencies (Bitcoin, Ethereum), CBDCs are

centralized, government-backed, and represent a state-sponsored alternative to private digital assets.

CBDCs aim to combine the efficiency of digital payments with the stability of traditional currency. Motivations include:

Financial inclusion: Providing digital payments to unbanked populations

Payment efficiency: Reducing costs of cash handling and cross-border transfers

Monetary control: Preserving central bank authority amid declining cash usage and private stablecoin adoption

Projects range from China’s e-CNY (most advanced) to Europe’s digital euro and the U.S. exploring a digital dollar. Critics warn CBDCs enable surveillance, programmable money (expiration dates, spending restrictions), and financial exclusion if poorly designed. The cypherpunk movement views CBDCs as antithetical to decentralization—state-controlled alternatives directly opposing the privacy and autonomy principles underlying cryptocurrency. The ideological tension between CBDCs and decentralized crypto defines a central axis of the future monetary system debate.

The Philosophical Debate: Privacy, Control, and Financial Sovereignty

At the heart of the cryptocurrency movement lies a profound

philosophical debate between

privacy, control, and financial sovereignty—pitting decentralized ideals against state-backed systems.

Financial sovereignty advocates argue that individuals should have absolute control over their assets without intermediaries. Self-custody—holding one’s own private keys—embodies this principle. Bitcoin emerged as a response to the 2008 financial crisis, offering censorship-resistant, borderless value transfer immune to bailouts and monetary manipulation.

Privacy remains contentious. While cypherpunks envisioned fully anonymous digital cash, most major cryptocurrencies today offer

pseudonymity, not privacy. Regulators demand anti-money laundering (AML) and know-your-customer (KYC) compliance, pressuring exchanges and protocols. Privacy coins (Monero, Zcash) face delisting and regulatory hostility, reflecting the tension between individual privacy rights and state surveillance imperatives.

Control manifests in the battle between decentralized protocols and centralized institutions. Decentralized finance (DeFi) enables permissionless lending and trading; regulators increasingly target it for consumer protection. Central Bank Digital Currencies (CBDCs) represent the state’s response—programmable money that could enforce compliance, sunset provisions, or surveillance capabilities antithetical to crypto’s founding ethos.

This debate transcends technology: it questions whether money should be a neutral, open protocol (like the internet) or a state-managed instrument of policy. The outcome will shape financial systems, individual autonomy, and the balance of power between citizens and institutions for generations.

How CBDCs Could Coexist (or Conflict) with Bitcoin and Ethereum

The coexistence of Central Bank Digital Currencies (CBDCs) and decentralized cryptocurrencies like Bitcoin and Ethereum will likely involve both integration and conflict, reflecting deeper ideological divides.

Coexistence scenarios envision CBDCs operating alongside crypto as complementary layers. CBDCs could provide regulated on-ramps—central bank money tokenized on public blockchains, enabling compliant DeFi applications. Ethereum’s programmability might integrate CBDCs as stable assets within decentralized ecosystems, with bridges ensuring interoperability. Institutional investors might hold Bitcoin as “digital gold” while using CBDCs for everyday payments.

Conflict scenarios arise from fundamental tensions. Governments could use CBDCs to restrict crypto adoption—limiting on-ramps, taxing self-custody wallets out of existence, or banning private cryptocurrencies entirely. CBDCs enable programmable restrictions (expiring funds, spending limits) directly opposed to Bitcoin’s censorship resistance. Privacy advocates warn CBDCs could eliminate cash alternatives, forcing citizens into surveilled digital currencies.

The outcome depends on regulatory frameworks, technological choices, and political will. The most likely path is uneven global adoption, with some jurisdictions embracing crypto-CBDC coexistence and others pursuing outright crypto prohibition.

The Enduring Questions & Conclusion

Regulation vs. Innovation: Finding a Global Equilibrium

The tension between regulation and innovation defines cryptocurrency’s path forward. Overregulation risks stifling technological advancement, driving development to hostile jurisdictions, and undermining decentralization. Underregulation enables fraud, consumer losses, and systemic risks (as seen with FTX).

Finding global equilibrium requires frameworks that:

Protect consumers without imposing impossible compliance burdens

–Preserve innovation through regulatory sandboxes and clear token classifications

Enable compliance via on-chain monitoring rather than forcing off-chain intermediaries

Harmonize internationally to prevent regulatory arbitrage

The EU’s MiCA exemplifies comprehensive yet innovation-aware regulation. The U.S. faces criticism for “regulation-by-enforcement.” Emerging economies balance crypto adoption for financial inclusion against monetary control. Achieving equilibrium remains elusive but essential—neither unchecked speculation nor prohibitive control serves the technology’s potential to create more open, inclusive financial infrastructure.

Environmental Impact: Proof-of-Stake, Renewable Mining, and the ESG Debate

Cryptocurrency’s environmental impact became a defining controversy during Bitcoin’s energy consumption peak in 2021, sparking the ESG (Environmental, Social, Governance) debate that influenced institutional adoption.

Bitcoin mining’s energy use—comparable to small countries—drew criticism. However, the industry shifted significantly toward renewable energy, with estimates suggesting 50-60% of mining now uses sustainable sources (stranded hydro, flare gas, nuclear). Mining also stabilizes renewable grids by monetizing excess energy.

Proof-of-Stake (PoS) networks like Ethereum post-Merge reduced energy consumption by ~99.9%, eliminating environmental objections for PoS blockchains. This transition enabled ESG-conscious institutions to engage with Ethereum while Bitcoin maintained Proof-of-Work with renewable-heavy energy profiles.

The ESG debate now nuances: critics still target Bitcoin’s absolute energy use; proponents argue energy consumption isn’t inherently harmful if renewable-sourced and secures a decentralized global monetary network. Emerging solutions include mining methane (turning waste into energy), stranded energy utilization, and carbon offset initiatives. The industry increasingly frames energy use as a trade-off for censorship resistance and decentralized security rather than environmental negligence.

The Ultimate Use Case: Is Crypto a Currency, a Commodity, a Technology Platform, or an Asset Class?

Cryptocurrency defies simple categorization, simultaneously functioning as currency, commodity, technology platform, and asset class—a hybrid nature that fuels both innovation and regulatory confusion.

Currency: Bitcoin was designed as peer-to-peer electronic cash; cryptocurrencies enable borderless value transfer.

Commodity: Like gold, Bitcoin is mined, scarce, and treated as a store of value by regulators (SEC labels Bitcoin a commodity).

Technology Platform: Ethereum and other smart contract platforms enable decentralized applications, making them programmable infrastructure.

Asset Class: Institutions treat crypto as an investable asset with distinct risk-return profiles.

This multiplicity is crypto’s strength and regulatory challenge—it cannot be forced into traditional legal boxes, demanding new frameworks recognizing its layered nature.

Conclusion: From Cypherpunk Dream to Global Infrastructure—The Unfinished Revolution

The journey from the Cypherpunk dream of the 1980s to today’s global crypto infrastructure represents one of technology’s most consequential revolutions—yet remains fundamentally unfinished. What began as a fringe movement of cryptographers advocating for privacy and decentralized systems has matured into a trillion-dollar industry spanning digital currency, smart contract platforms, DeFi, NFTs, and institutional adoption.

This evolution achieved milestones once unimaginable: Bitcoin survived a decade and a half, Ethereum became a global settlement layer, and governments now debate Central Bank Digital Currencies in response. However, the revolution’s core promises—true privacy, genuine decentralization, and universal financial access—remain contested and incomplete.

The path forward faces unresolved tensions: regulation vs. innovation, scalability vs. decentralization, institutional integration vs. cypherpunk ideals. The coming years will determine whether crypto becomes another captured, regulated financial layer or fulfills its original vision of permissionless, censorship-resistant, user-sovereign infrastructure. Regardless of outcome, the Cypherpunk movement succeeded in altering the trajectory of money, technology, and individual autonomy—proving that ideas incubated on mailing lists can reshape the global financial order. The revolution continues.